Mortgage Calculator

Calculate your monthly mortgage payment and total interest

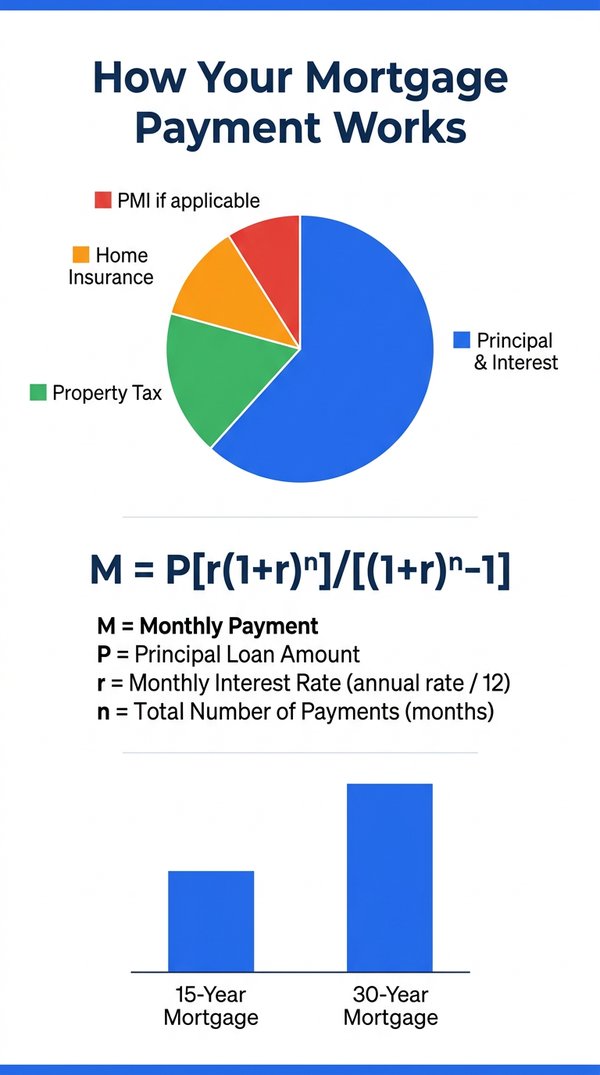

Mortgage Payment Formula

- M = Monthly payment

- P = Principal loan amount

- r = Monthly interest rate (annual rate / 12)

- n = Number of payments (loan term × 12)

How to Calculate Your Mortgage Payment

Use this mortgage calculator to estimate your monthly payment and total interest over the life of your loan. Follow these steps:

- Enter the home price — the total purchase price of the property you want to buy.

- Add your down payment — the upfront cash you pay. A larger down payment means a smaller loan and lower monthly payments. Most lenders require at least 3-5% down, but 20% eliminates PMI.

- Input the interest rate — the annual percentage rate (APR) your lender charges. Even a 0.5% difference can save or cost thousands over the life of the loan.

- Choose your loan term — typically 15 or 30 years. Shorter terms have higher monthly payments but much less total interest.

- Include property tax and insurance — these are often escrowed into your monthly payment (PITI: Principal, Interest, Tax, Insurance).

Example: For a $350,000 home with $70,000 down (20%), a 6.5% interest rate on a 30-year term, your monthly principal and interest would be approximately $1,769. With $3,500/year property tax and $1,200/year insurance, your total monthly payment would be about $2,144.

Complete Guide to Understanding Mortgages

What Is a Mortgage?

A mortgage is a loan used to purchase real estate, where the property itself serves as collateral. When you buy a home, you typically don't pay the full price upfront. Instead, you make a down payment (usually 3-20% of the purchase price) and borrow the rest from a lender. The mortgage is repaid over a set period — commonly 15 or 30 years — through monthly payments that include both principal (the amount borrowed) and interest (the cost of borrowing).

How Do Mortgage Payments Work?

Each monthly mortgage payment is divided into four components, often referred to as PITI:

- Principal (P): The portion that reduces your outstanding loan balance

- Interest (I): The lender's charge for borrowing money

- Tax (T): Property taxes collected by your local government

- Insurance (I): Homeowner's insurance and possibly Private Mortgage Insurance (PMI)

In the early years of your mortgage, most of your payment goes toward interest. Over time, this shifts — a process called amortization. By the final years of your loan, nearly all of each payment goes toward building equity in your home.

Types of Mortgages Explained

Understanding the different mortgage types is crucial for making the right choice:

Fixed-Rate Mortgages

- 30-Year Fixed: Most popular choice. Lower monthly payments, but more total interest over the life of the loan. Best for buyers who plan to stay in their home long-term.

- 15-Year Fixed: Higher monthly payments, but 50-60% less total interest. Ideal for buyers who can afford higher payments and want to build equity faster.

- 20-Year or 10-Year Fixed: Less common options that offer a middle ground or accelerated payoff.

Adjustable-Rate Mortgages (ARMs)

- 5/1 ARM: Fixed rate for 5 years, then adjusts annually. Lower initial rate, but risk of increases later.

- 7/1 ARM: Fixed for 7 years before adjusting. Good middle ground for medium-term ownership.

- 10/1 ARM: Fixed for 10 years. Suitable if you plan to sell or refinance within a decade.

Government-Backed Loans

- FHA Loans: Backed by the Federal Housing Administration. Require as little as 3.5% down. More lenient credit requirements.

- VA Loans: For veterans and active military. Often require zero down payment and no PMI.

- USDA Loans: For rural homebuyers. May offer 100% financing with income limits.

Current Mortgage Rate Trends (2026)

Mortgage rates fluctuate based on economic conditions, Federal Reserve policy, and bond market movements. Here's a general overview of recent trends:

| Loan Type | Typical Rate Range | Best For |

|---|---|---|

| 30-Year Fixed | 6.0% - 7.5% | Long-term stability |

| 15-Year Fixed | 5.25% - 6.75% | Faster equity building |

| 5/1 ARM | 5.5% - 6.5% | Short-term ownership |

| FHA 30-Year | 5.75% - 7.0% | First-time buyers |

| VA 30-Year | 5.5% - 6.75% | Veterans & military |

Rates shown are approximate and vary by lender, credit score, and market conditions. Always shop around for the best rate.

Understanding Your Debt-to-Income Ratio (DTI)

Your DTI ratio is one of the most important factors lenders consider when approving your mortgage. It measures how much of your monthly income goes toward debt payments:

Formula: DTI = (Total Monthly Debt Payments / Gross Monthly Income) × 100

Example: If you earn $6,000/month and have $1,800 in total debt payments (including your new mortgage), your DTI is 30%.

| DTI Ratio | Lender Perception | Likely Outcome |

|---|---|---|

| Below 28% | Excellent | Best rates available |

| 28% - 36% | Good | Standard approval |

| 36% - 43% | Acceptable | May need larger down payment |

| Above 43% | High Risk | Approval difficult |

Real-World Mortgage Case Studies

Case Study 1: First-Time Homebuyer — The Johnson Family

Situation:

- Home Price: $350,000

- Down Payment: $70,000 (20%)

- Loan Amount: $280,000

- Interest Rate: 6.5%

- Loan Term: 30 years

Results:

- Monthly Principal & Interest: $1,769

- Property Tax + Insurance: $450/month

- Total Monthly Payment: $2,219

- Total Interest Over 30 Years: $356,966

- Total Cost of Home: $706,966

Key Takeaway: By putting 20% down, the Johnsons avoided PMI (saving ~$200/month). However, they'll pay $356,966 in interest over 30 years — more than the original loan amount. If they had chosen a 15-year term at 5.75%, they would save over $180,000 in interest.

Case Study 2: 15-Year vs 30-Year Comparison — Sarah's Decision

| Factor | 30-Year @ 6.5% | 15-Year @ 5.75% |

|---|---|---|

| Loan Amount | $280,000 | $280,000 |

| Monthly P&I | $1,769 | $2,324 |

| Total Interest | $356,966 | $138,349 |

| Total Cost | $636,966 | $418,349 |

| Interest Savings | — | $218,617 |

Key Takeaway: The 15-year mortgage costs $555 more per month, but saves $218,617 in total interest. If Sarah can comfortably afford the higher payment, the 15-year option builds equity faster and saves a fortune. If cash flow is tight, the 30-year option provides flexibility — she can always make extra payments when possible.

Case Study 3: The Power of Extra Payments — Mike's Strategy

Situation: Mike has a $300,000 mortgage at 6.5% for 30 years. His regular monthly payment is $1,896. Instead of making just the minimum, Mike decides to pay an extra $200 each month toward principal.

Impact of Extra $200/Month:

- Original payoff date: 30 years

- New payoff date: 22 years, 4 months

- Time saved: 7 years, 8 months

- Interest saved: ~$89,000

Key Takeaway: Even modest extra payments can dramatically reduce your loan term and total interest. Consider biweekly payments (26 half-payments per year = 13 full payments), rounding up to the nearest hundred, or applying tax refunds or bonuses directly to principal.

Expert Tips for Getting the Best Mortgage Rate

Your mortgage rate can vary by 0.5% to 1% or more depending on your financial profile and market conditions. Here are proven strategies to secure the lowest possible rate:

1. Improve Your Credit Score

Your credit score is the #1 factor affecting your rate. A score of 760+ typically gets the best rates. To improve: pay all bills on time, reduce credit card balances below 30% of limits, avoid opening new credit accounts before applying, and check your report for errors.

2. Save for a Larger Down Payment

A 20% down payment eliminates PMI and often qualifies you for better rates. Even going from 5% to 10% down can improve your rate by 0.25-0.5%. Consider using gift funds, selling assets, or tapping retirement accounts (with caution) for a larger down payment.

3. Shop Multiple Lenders

Rates can vary by 0.5% or more between lenders. Get quotes from at least 3-5 lenders — including banks, credit unions, and online lenders. Compare Loan Estimates (LE) side by side, looking at both rate and closing costs. Don't forget to ask about lender credits or discount points.

4. Consider Buying Points

Discount points let you "buy down" your rate. Each point costs 1% of the loan amount and typically reduces your rate by 0.25%. If you pay $3,000 for a point that saves $100/month, you break even in 30 months. If you plan to stay in the home longer, points can be a smart investment.

5. Lower Your Debt-to-Income Ratio

Lenders prefer DTI below 36%. Before applying, pay down credit card balances, avoid taking on new debt (like car loans), and consider increasing your down payment to reduce the loan amount. A lower DTI not only improves approval odds but can also qualify you for better rates.

6. Lock Your Rate at the Right Time

Mortgage rates change daily — sometimes multiple times per day. Once you have a rate you're happy with, ask your lender about a rate lock (typically 30-60 days). This guarantees your rate won't increase before closing, even if market rates rise. Some lenders offer "float down" options if rates drop.

Pro Tip: A 0.5% rate difference on a $300,000, 30-year mortgage saves you $32,000+ over the life of the loan. That's why shopping around and improving your financial profile before applying is one of the most impactful things you can do.

Common Mortgage Mistakes to Avoid

Not Getting Pre-Approved First

Many buyers start house hunting before getting pre-approved. This wastes time and weakens your negotiating position. A pre-approval letter shows sellers you're a serious buyer and lets you shop within your actual budget. Get pre-approved before you start looking.

Making Large Purchases Before Closing

After your loan is approved but before closing, avoid buying furniture, opening credit cards, or making other large purchases. Lenders do a final credit check before closing, and new debt can derail your approval or change your rate.

Only Looking at the Monthly Payment

A lower monthly payment doesn't always mean a better deal. A 30-year mortgage has lower payments but costs far more in total interest than a 15-year. Always compare the total cost of the loan, not just the monthly payment. Use our calculator above to see both.

Skipping the Home Inspection

Even in a competitive market, never waive the home inspection. A thorough inspection can reveal costly issues (roof damage, foundation problems, outdated electrical) that could save you thousands. The $300-500 inspection fee is a smart investment.

Not Budgeting for Closing Costs

Closing costs typically run 2-5% of the home price ($7,000-$17,500 on a $350,000 home). These include appraisal fees, title insurance, attorney fees, and prepaid taxes and insurance. Budget for these costs upfront so you're not caught off guard at closing.

Ignoring the APR When Comparing Loans

The interest rate doesn't tell the whole story. The APR includes the interest rate plus fees and costs, giving you the true cost of borrowing. When comparing two loans, the one with the lower APR is usually the better deal — even if its interest rate is slightly higher.

Frequently Asked Questions

How much house can I afford?

A common guideline is the 28/36 rule: spend no more than 28% of your gross monthly income on housing costs (mortgage, taxes, insurance) and no more than 36% on total debt. For example, with a $6,000 monthly gross income, your maximum mortgage payment should be around $1,680. Also factor in your down payment, credit score, and other financial obligations.

What is the difference between APR and interest rate?

The interest rate is the cost of borrowing the principal loan amount. The APR (Annual Percentage Rate) includes the interest rate plus other costs like origination fees, closing costs, and mortgage insurance. APR gives you a more complete picture of the total cost of the loan, making it easier to compare offers from different lenders.

How does a down payment affect my mortgage?

A larger down payment reduces your loan amount, which lowers your monthly payment and total interest paid. Putting down at least 20% eliminates the need for Private Mortgage Insurance (PMI), saving you 0.5-1% of the loan amount annually. Even a 5% increase in your down payment can significantly reduce your long-term costs.

Should I choose a 15-year or 30-year mortgage?

A 15-year mortgage has higher monthly payments but saves substantially on total interest — often 50-60% less than a 30-year loan. A 30-year mortgage offers lower monthly payments and more financial flexibility. Choose 15 years if you can comfortably afford the higher payments and want to build equity faster; choose 30 years if you need lower payments or want to invest the difference elsewhere.

What is PMI and when can I remove it?

Private Mortgage Insurance (PMI) is required when your down payment is less than 20%. It typically costs 0.5-1% of the loan amount per year. By law, your lender must cancel PMI when your mortgage balance reaches 78% of the original home value. You can also request early cancellation once you reach 80% loan-to-value through payments or home appreciation.

How much of my mortgage payment goes to principal vs interest?

In the early years of a mortgage, most of your payment goes toward interest (often 70-80%). Over time, the ratio gradually shifts as you pay down the principal. This is called amortization. For a $280,000 loan at 6.5% over 30 years, your first payment might be $1,769 with only $252 going to principal. By the final year, nearly all of each payment goes to principal.

What are closing costs and how much should I expect to pay?

Closing costs are fees paid at the closing of your home purchase, typically 2-5% of the home price. They include appraisal fees, title insurance, attorney fees, origination fees, recording fees, and prepaid property taxes and insurance. On a $350,000 home, expect closing costs of $7,000-$17,500. You can sometimes negotiate for the seller to cover part of these costs.

Should I buy discount points to lower my rate?

Discount points let you pay upfront to reduce your interest rate. Each point costs 1% of the loan amount and typically lowers your rate by 0.25%. To decide if points make sense, calculate your break-even point: divide the cost of points by your monthly savings. If you plan to stay in the home longer than the break-even period, buying points can save you money over time.

What credit score do I need to get a mortgage?

Conventional loans typically require a minimum credit score of 620, though scores of 740+ get the best rates. FHA loans accept scores as low as 580 (or even 500 with a 10% down payment). VA loans have no minimum score set by the VA, but lenders often require 620+. Higher scores mean better rates — improving your score from 680 to 760 can save tens of thousands over the life of the loan.

Can I get a mortgage if I'm self-employed?

Yes, but the process is more involved. Self-employed borrowers typically need to provide 2 years of tax returns, profit-and-loss statements, and possibly bank statements. Lenders look at your net income after business expenses, so deductions that reduce your taxable income can also reduce your qualifying income. Consider working with a mortgage broker who specializes in self-employed borrowers.

How does refinancing work and when should I do it?

Refinancing replaces your current mortgage with a new one, usually to get a lower rate or shorter term. The general rule is to refinance if you can lower your rate by at least 0.5-1%. Consider refinancing when rates drop significantly, your credit score has improved, you want to switch from an ARM to a fixed rate, or you want to cash out home equity. Factor in closing costs ($3,000-$6,000) and calculate your break-even point.

What is an escrow account and do I need one?

An escrow account is managed by your lender to pay property taxes and homeowner's insurance on your behalf. Your monthly payment includes 1/12 of the annual tax and insurance costs, which the lender holds in escrow. Most lenders require escrow if your down payment is less than 20%. While it increases your monthly payment slightly, it ensures these bills are paid on time and protects both you and the lender.